Bayesian BLP on the Nevo (2000) Cereal Panel#

This notebook applies BayesianBLP to the canonical aggregate-share demand dataset from Nevo’s “A Practitioner’s Guide to Estimation of Random Coefficients Logit Models of Demand”: 24 ready-to-eat cereal brands across 47 US cities × 2 quarters, with prices, two product characteristics (sugar content, mushy indicator), and Nevo’s five Hausman-style instruments (z6..z10).

We will:

Load and clean the public Nevo panel.

Synthesize the outside-good rows (Nevo’s data ships without one).

Fit

BayesianBLPwithnutpieon a tractable subset of cities.Check posterior diagnostics (\(\hat{R}\) and ESS).

Show the IV correction holds on real data.

Inspect own-price elasticities and run two counterfactuals (panel-wide and time-targeted).

Read the per-market taste profiles to see which consumer types each market relies on.

Note on the data. Nevo (2000) states that the Practitioner’s Guide dataset is simulated data calibrated to the cereal market, not actual scanner data. The real empirical results are in Nevo (2001, Econometrica). We use the simulated panel because it is the standard teaching example.

Before you read this notebook. The methodology, prior structure, IV decomposition, hierarchical pooling, and counterfactual mechanics are introduced in

bayesian_blp.ipynbusing a synthetic panel with known truth. This notebook assumes you have read that one. Here we apply the same model to the canonical empirical dataset and check that it reproduces the elasticity range published in the literature.

import time

import warnings

import arviz as az

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from pymc_marketing.customer_choice import BayesianBLP, taste_profiles

warnings.filterwarnings("ignore")

az.style.use("arviz-darkgrid")

plt.rcParams["figure.figsize"] = [10, 4]

plt.rcParams["figure.dpi"] = 110

%config InlineBackend.figure_format = 'retina'

1. Load and inspect the Nevo panel#

The CSV ships with European decimal formatting ("," as the decimal separator), so we pass decimal="," to pd.read_csv. The raw layout is inside-products only: the outside good’s share is implicit, equal to 1 - sum(inside_shares) per market.

from pymc_marketing.paths import data_dir

raw = pd.read_csv(data_dir / "data_nevo.csv", decimal=",")

# Compose city x quarter -> (region, period). The original file has only

# year=88 and quarters 1, 2, so 47 cities x 2 quarters = 94 markets.

raw["period"] = raw["year"].astype(int) * 4 + raw["quarter"].astype(int)

raw["region"] = "c" + raw["city"].astype(str)

raw["market"] = raw["region"] + "_" + raw["period"].astype(str)

# Decode firm codes to readable names

FIRM_NAMES = {

1: "Kelloggs",

2: "GenMills",

3: "Post",

4: "Quaker",

6: "Ralston",

}

raw["firm_name"] = raw["firm"].map(FIRM_NAMES)

raw["product"] = raw["firm_name"] + "_" + raw["brand"].astype(int).astype(str)

print(f"Rows: {len(raw)}")

print(f"Brands: {raw['firmbr'].nunique()}")

print(f"Cities: {raw['city'].nunique()}")

print(f"Quarters: {sorted(raw['quarter'].unique())}")

print(f"Markets (city × period): {raw.groupby(['city', 'period']).ngroups}")

market_share_sums = raw.groupby("market")["share"].sum()

print(

f"\nInside-share sum per market: "

f"mean={market_share_sums.mean():.3f}, "

f"min={market_share_sums.min():.3f}, "

f"max={market_share_sums.max():.3f}"

)

print(

"→ Outside-good share averages "

f"~{1 - market_share_sums.mean():.2f}; "

"we synthesize one outside row per market below."

)

raw.head(4)

Rows: 2256

Brands: 24

Cities: 47

Quarters: [np.int64(1), np.int64(2)]

Markets (city × period): 94

Inside-share sum per market: mean=0.476, min=0.185, max=0.696

→ Outside-good share averages ~0.52; we synthesize one outside row per market below.

| id | firmbr | firm | brand | city | year | quarter | share | price | sugar | ... | z16 | z17 | z18 | z19 | z20 | period | region | market | firm_name | product | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 100401880 | 1004 | 1 | 4 | 1 | 88 | 1 | 0.0124 | 0.072 | 2.0 | ... | 0.067 | 0.068 | 0.035 | 0.126 | 0.035 | 353 | c1 | c1_353 | Kelloggs | Kelloggs_4 |

| 1 | 100601880 | 1006 | 1 | 6 | 1 | 88 | 1 | 0.0078 | 0.114 | 18.0 | ... | 0.088 | 0.111 | 0.088 | 0.050 | 0.073 | 353 | c1 | c1_353 | Kelloggs | Kelloggs_6 |

| 2 | 100701880 | 1007 | 1 | 7 | 1 | 88 | 1 | 0.0130 | 0.132 | 4.0 | ... | 0.112 | 0.108 | 0.086 | 0.122 | 0.102 | 353 | c1 | c1_353 | Kelloggs | Kelloggs_7 |

| 3 | 100901880 | 1009 | 1 | 9 | 1 | 88 | 1 | 0.0058 | 0.130 | 3.0 | ... | 0.088 | 0.102 | 0.102 | 0.111 | 0.104 | 353 | c1 | c1_353 | Kelloggs | Kelloggs_9 |

4 rows × 36 columns

2. Build the BayesianBLP input#

Three transformations:

Subset. The full 94-market × 24-brand panel produces a 2256-cell \(\tilde{\xi}\) block whose joint geometry with \((\rho, \sigma_\xi)\) makes a CPU fit expensive (≈15 min). We subset to 8 cities × 2 quarters = 16 markets so the notebook fits in a few minutes. The methodology is identical at full scale.

Rescale price. Nevo’s published price scale is “share of category dollar sales per serving” (≈0.05–0.22). The default

α ~ Normal(0, 2)prior assumes a roughly unit-variance price scale, so on the raw Nevo scale the implied \(\alpha \cdot p\) term in utility is too small and the posterior collapses to near-zero own-price elasticities. We multiply price by 100 (cents) so \(|\alpha|\) naturally lands in the prior support.Synthesize outside rows. One row per market and time,

share = 1 - Σ(inside), all characteristics, instruments, and price set to zero. This matches the convention used by the synthetic-data generator.

Caveat on the fabricated market size (

n=1,000). Nevo’s dataset reports market shares but not market sizes (number of potential consumers). The log-share-ratio likelihood needs a per-cell variance scale, so we fill in a constantn=1,000. This is a methodological placeholder: posterior elasticity magnitudes scale with the assumedn, so absolute levels are not directly comparable with published Nevo results. Substitution patterns and elasticity ratios are unaffected.

N_CITIES_DEMO = 8

# Nevo's five Hausman-style instruments: prices of the same brand in

# other markets (z6..z10). The wider 20-instrument set is also available

# but adds little identifying variation for the diagonal-RC specification

# used here, so we match Nevo's original identification strategy.

INSTRUMENTS = [f"z{i}" for i in range(6, 11)]

# Subset to N_CITIES_DEMO cities x 2 quarters x 24 brands.

keep_cities = sorted(raw["city"].unique())[:N_CITIES_DEMO]

df_inside = raw[raw["city"].isin(keep_cities)].copy()

df_inside["price"] = df_inside["price"] * 100.0 # to cents

# Synthesize outside-good rows

market_share_sum = df_inside.groupby("market")["share"].sum()

outside_share = 1.0 - market_share_sum

market_meta = df_inside.drop_duplicates("market").set_index("market")[

["region", "period"]

]

outside = pd.DataFrame(

{

"market": outside_share.index,

"product": "outside",

"share": outside_share.values,

"price": 0.0,

"sugar": 0.0,

"mushy": 0.0,

**{c: 0.0 for c in INSTRUMENTS},

}

)

outside["region"] = market_meta.reindex(outside["market"])["region"].values

outside["period"] = market_meta.reindex(outside["market"])["period"].values

# n_jt is required by the log-share-ratio likelihood as a per-cell

# variance scale, but Nevo's data does not include serving counts.

# We assign a *fabricated* constant n=1,000 so the likelihood is

# well-defined. Caveat: elasticity magnitudes scale with the implied

# variance, so absolute levels here should NOT be compared with

# published Nevo estimates. Patterns and ratios remain interpretable.

df_inside["n"] = 1000

outside["n"] = 1000

df = pd.concat([df_inside, outside], ignore_index=True, sort=False)

assert np.allclose(df.groupby("market")["share"].sum(), 1.0, atol=1e-6) # noqa: S101

print(

f"Final long-format frame: {len(df)} rows "

f"(= {df['market'].nunique()} markets x {df['product'].nunique()} products)"

)

df[

["market", "region", "period", "product", "share", "price", "sugar", "mushy", "n"]

].head(6)

Final long-format frame: 400 rows (= 16 markets x 25 products)

| market | region | period | product | share | price | sugar | mushy | n | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | c1_353 | c1 | 353 | Kelloggs_4 | 0.0124 | 7.2 | 2.0 | 1.0 | 1000 |

| 1 | c1_353 | c1 | 353 | Kelloggs_6 | 0.0078 | 11.4 | 18.0 | 1.0 | 1000 |

| 2 | c1_353 | c1 | 353 | Kelloggs_7 | 0.0130 | 13.2 | 4.0 | 1.0 | 1000 |

| 3 | c1_353 | c1 | 353 | Kelloggs_9 | 0.0058 | 13.0 | 3.0 | 0.0 | 1000 |

| 4 | c1_353 | c1 | 353 | Kelloggs_11 | 0.0179 | 15.5 | 12.0 | 0.0 | 1000 |

| 5 | c1_353 | c1 | 353 | Kelloggs_13 | 0.0266 | 13.7 | 14.0 | 0.0 | 1000 |

3. Construct and fit the model#

We declare region_col="region" and time_col="period" so cities pool hierarchically on \(\alpha_r\), and the period coordinate is exposed for time-targeted counterfactuals. The five instruments enable the conditional decomposition \(\tilde{\xi} \mid \eta \sim N(\rho \sigma_\xi / \sigma_\eta \cdot \eta, \, \sigma_\xi \sqrt{1-\rho^2})\) that corrects for price endogeneity, the headline empirical concern in Nevo’s paper.

from pymc_extras.prior import Prior

model = BayesianBLP(

market_data=df,

characteristics=["sugar", "mushy"],

instruments=INSTRUMENTS,

region_col="region",

time_col="period",

random_coef_on=["price", "sugar", "mushy"],

n_mc_draws=200,

model_config={

"sigma_xi": Prior("HalfNormal", sigma=0.5),

"sigma_xi_j": Prior("HalfNormal", sigma=0.25),

"alpha": Prior("Normal", mu=0.0, sigma=3.0), # slightly wider prior

},

random_seed=0,

hierarchical_parameterisation="noncentered",

)

print(

f"M={model._M} markets, J={model._J} inside products, "

f"R={len(model._regions)} regions, T={model._T} periods, "

f"K={model._K} characteristics, L={model._L} instruments"

)

print(

f"Halton grid shape: {model._halton.shape} (random_coef_on={model._random_coef_names})"

)

M=16 markets, J=24 inside products, R=8 regions, T=2 periods, K=2 characteristics, L=5 instruments

Halton grid shape: (200, 3) (random_coef_on=['price', 'sugar', 'mushy'])

t0 = time.perf_counter()

model.fit(

nuts_sampler="nutpie",

draws=2000,

tune=1000,

chains=4,

target_accept=0.95,

progressbar=True,

init="adapt_full",

random_seed=0,

)

elapsed = time.perf_counter() - t0

n_div = int(model.idata.sample_stats["diverging"].sum())

print(f"\nFit took {elapsed:.0f}s ({elapsed / 60:.1f} min). Divergences: {n_div}")

Sampler Progress

Total Chains: 4

Active Chains: 0

Finished Chains: 4

Sampling for 4 minutes

Estimated Time to Completion: now

| Progress | Draws | Divergences | Step Size | Gradients/Draw |

|---|---|---|---|---|

| 3000 | 0 | 0.08 | 63 | |

| 3000 | 0 | 0.07 | 63 | |

| 3000 | 0 | 0.08 | 127 | |

| 3000 | 0 | 0.07 | 63 |

Fit took 309s (5.2 min). Divergences: 0

4. Posterior diagnostics#

# a) Headline summary on the parameters that drive predictions

az.summary(

model.idata,

var_names=[

"alpha_pop",

"beta_pop",

"tau_alpha",

"sigma_random",

"rho_price_xi",

"sigma_xi",

"sigma_xi_j",

],

)

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| alpha_pop | -0.328 | 0.036 | -0.394 | -0.257 | 0.002 | 0.001 | 259.0 | 491.0 | 1.01 |

| beta_pop[sugar] | 0.030 | 0.029 | -0.026 | 0.084 | 0.001 | 0.001 | 416.0 | 768.0 | 1.02 |

| beta_pop[mushy] | -0.245 | 0.315 | -0.822 | 0.379 | 0.014 | 0.008 | 516.0 | 840.0 | 1.02 |

| tau_alpha | 0.070 | 0.029 | 0.030 | 0.120 | 0.001 | 0.001 | 468.0 | 1018.0 | 1.00 |

| sigma_random[price] | 0.149 | 0.028 | 0.094 | 0.197 | 0.001 | 0.001 | 731.0 | 1206.0 | 1.01 |

| sigma_random[sugar] | 0.034 | 0.024 | 0.000 | 0.078 | 0.001 | 0.000 | 1474.0 | 891.0 | 1.00 |

| sigma_random[mushy] | 0.285 | 0.213 | 0.000 | 0.668 | 0.003 | 0.002 | 2787.0 | 1696.0 | 1.00 |

| rho_price_xi | 0.336 | 0.125 | 0.104 | 0.568 | 0.004 | 0.002 | 1122.0 | 2204.0 | 1.00 |

| sigma_xi | 0.749 | 0.050 | 0.661 | 0.844 | 0.001 | 0.001 | 1346.0 | 2341.0 | 1.00 |

| sigma_xi_j | 0.727 | 0.094 | 0.561 | 0.904 | 0.004 | 0.002 | 711.0 | 1473.0 | 1.01 |

Read this table for two things:

\(\hat{R}\) close to 1 (≤ 1.02 ideal). Values 1.05–1.20 indicate chains that haven’t fully mixed. For a tutorial fit with 2 chains × 1500 steps this is acceptable; for production inference run 4 chains × 2000 draws.

ess_bulkshould be ≥ 100 for parameters you want to report. The characteristic coefficients (beta_pop[sugar],beta_pop[mushy]) often have lower ESS thanalpha_pophere. This is structural: there are only J=24 brand-level draws of each characteristic per market, vs J×R = 24×R draws of price.

5. Endogeneity correction holds up on Nevo#

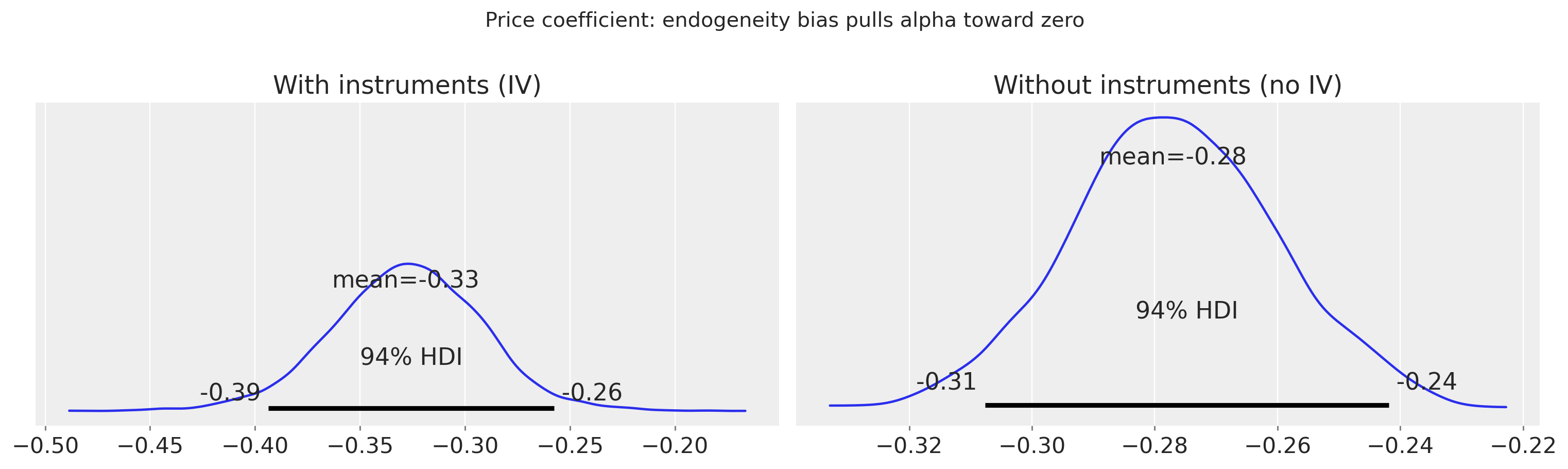

The synthetic notebook showed that dropping instruments biases \(\alpha\) toward zero by a known amount. The same comparison on Nevo serves as a real-data check: if the IV correction is doing its job, the no-IV fit produces a price coefficient closer to zero, and the IV fit’s \(\rho_{\text{price},\xi}\) should sit away from zero in the posterior.

# Fit without instruments to show endogeneity bias

with warnings.catch_warnings():

warnings.simplefilter("ignore")

model_noiv = BayesianBLP(

market_data=df,

characteristics=["sugar", "mushy"],

instruments=None,

random_coef_on=["price", "sugar", "mushy"],

n_mc_draws=200,

model_config={

"sigma_xi": Prior("HalfNormal", sigma=0.5),

"sigma_xi_j": Prior("HalfNormal", sigma=0.25),

"alpha": Prior("Normal", mu=0.0, sigma=3.0),

},

random_seed=0,

hierarchical_parameterisation="noncentered",

)

model_noiv.fit(

nuts_sampler="nutpie",

draws=1000,

tune=1000,

chains=4,

target_accept=0.95,

progressbar=True,

init="adapt_full",

random_seed=0,

)

Sampler Progress

Total Chains: 4

Active Chains: 0

Finished Chains: 4

Sampling for 2 minutes

Estimated Time to Completion: now

| Progress | Draws | Divergences | Step Size | Gradients/Draw |

|---|---|---|---|---|

| 2000 | 0 | 0.09 | 31 | |

| 2000 | 0 | 0.09 | 127 | |

| 2000 | 0 | 0.08 | 127 | |

| 2000 | 0 | 0.09 | 127 |

-

<xarray.Dataset> Size: 52MB Dimensions: (chain: 4, draw: 1000, characteristic: 2, inside_product: 24, market: 16, sigma_random_log___dim_0: 3, random_coef: 3, region: 1) Coordinates: * chain (chain) int64 32B 0 1 2 3 * draw (draw) int64 8kB 0 1 2 3 4 ... 995 996 997 998 999 * characteristic (characteristic) object 16B 'sugar' 'mushy' * inside_product (inside_product) object 192B 'GenMills_15' ... ... * market (market) object 128B 'c1_353' ... 'c12_354' * sigma_random_log___dim_0 (sigma_random_log___dim_0) int64 24B 0 1 2 * random_coef (random_coef) object 24B 'price' 'sugar' 'mushy' * region (region) object 8B 'all' Data variables: (12/18) alpha (chain, draw) float64 32kB -0.3208 ... -0.3062 beta (chain, draw, characteristic) float64 64kB 0.06... sigma_xi_j_log__ (chain, draw) float64 32kB -0.1923 ... -0.2409 xi_j_raw (chain, draw, inside_product) float64 768kB -2.... sigma_xi_free_log__ (chain, draw) float64 32kB -0.2245 ... -0.3211 xi_tilde_raw (chain, draw, market, inside_product) float64 12MB ... ... ... xi_j (chain, draw, inside_product) float64 768kB -1.... sigma_xi (chain, draw) float64 32kB 0.7989 ... 0.7254 xi_tilde (chain, draw, market, inside_product) float64 12MB ... xi (chain, draw, market, inside_product) float64 12MB ... s_inside (chain, draw, market, inside_product) float64 12MB ... s_outside (chain, draw, market) float64 512kB 0.5433 ... ... Attributes: created_at: 2026-05-26T06:54:35.267230+00:00 arviz_version: 0.23.0 inference_library: nutpie inference_library_version: 0.16.8 sampling_time: 167.7150101661682 tuning_steps: 1000 -

<xarray.Dataset> Size: 340kB Dimensions: (chain: 4, draw: 1000) Coordinates: * chain (chain) int64 32B 0 1 2 3 * draw (draw) int64 8kB 0 1 2 3 4 5 ... 995 996 997 998 999 Data variables: (12/13) depth (chain, draw) uint64 32kB 5 6 5 5 5 5 ... 5 6 6 6 6 6 maxdepth_reached (chain, draw) bool 4kB False False ... False False index_in_trajectory (chain, draw) int64 32kB -14 -56 17 17 ... 7 -55 36 logp (chain, draw) float64 32kB -673.0 -672.5 ... -715.1 energy (chain, draw) float64 32kB 872.7 866.6 ... 913.4 889.2 energy_error (chain, draw) float64 32kB 0.08809 ... -0.09431 ... ... step_size_bar (chain, draw) float64 32kB 0.09651 0.09651 ... 0.09203 mean_tree_accept (chain, draw) float64 32kB 0.9227 0.9632 ... 0.9597 mean_tree_accept_sym (chain, draw) float64 32kB 0.8868 0.9451 ... 0.936 n_steps (chain, draw) uint64 32kB 31 127 31 31 ... 63 127 127 tuning (chain, draw) bool 4kB False False ... False False diverging (chain, draw) bool 4kB False False ... False False Attributes: created_at: 2026-05-26T06:54:35.241343+00:00 arviz_version: 0.23.0 -

<xarray.Dataset> Size: 5kB Dimensions: (market: 16, inside_product: 24) Coordinates: * market (market) <U7 448B 'c1_353' 'c3_353' ... 'c11_354' 'c12_354' * inside_product (inside_product) <U11 1kB 'GenMills_15' ... 'Ralston_18' Data variables: log_share_ratio (market, inside_product) float64 3kB -4.433 ... -2.757 Attributes: created_at: 2026-05-26T06:54:35.266557+00:00 arviz_version: 0.23.0 inference_library: pymc inference_library_version: 5.28.2 -

<xarray.Dataset> Size: 21kB Dimensions: (market: 16, inside_product: 24, characteristic: 2, mc_draw: 200, random_coef: 3) Coordinates: * market (market) <U7 448B 'c1_353' 'c3_353' ... 'c11_354' 'c12_354' * inside_product (inside_product) <U11 1kB 'GenMills_15' ... 'Ralston_18' * characteristic (characteristic) <U5 40B 'sugar' 'mushy' * mc_draw (mc_draw) int64 2kB 0 1 2 3 4 5 ... 194 195 196 197 198 199 * random_coef (random_coef) <U5 60B 'price' 'sugar' 'mushy' Data variables: price (market, inside_product) float64 3kB 11.2 11.5 ... 15.3 14.3 x (market, inside_product, characteristic) float64 6kB 4.0 ... n (market) float64 128B 1e+03 1e+03 1e+03 ... 1e+03 1e+03 inside_share (market, inside_product) float64 3kB 0.0066 ... 0.0343 outside_share (market) float64 128B 0.5555 0.5853 0.3315 ... 0.5559 0.5405 halton (mc_draw, random_coef) float64 5kB -1.287 -1.608 ... 1.898 Attributes: created_at: 2026-05-26T06:54:35.258379+00:00 arviz_version: 0.23.0 inference_library: pymc inference_library_version: 5.28.2 -

<xarray.Dataset> Size: 52MB Dimensions: (chain: 4, draw: 1000, characteristic: 2, inside_product: 24, market: 16, sigma_random_log___dim_0: 3, random_coef: 3, region: 1) Coordinates: * chain (chain) int64 32B 0 1 2 3 * draw (draw) int64 8kB 0 1 2 3 4 ... 995 996 997 998 999 * characteristic (characteristic) object 16B 'sugar' 'mushy' * inside_product (inside_product) object 192B 'GenMills_15' ... ... * market (market) object 128B 'c1_353' ... 'c12_354' * sigma_random_log___dim_0 (sigma_random_log___dim_0) int64 24B 0 1 2 * random_coef (random_coef) object 24B 'price' 'sugar' 'mushy' * region (region) object 8B 'all' Data variables: (12/18) alpha (chain, draw) float64 32kB -0.7433 ... -0.2886 beta (chain, draw, characteristic) float64 64kB -0.0... sigma_xi_j_log__ (chain, draw) float64 32kB -1.071 ... -0.08395 xi_j_raw (chain, draw, inside_product) float64 768kB -0.... sigma_xi_free_log__ (chain, draw) float64 32kB -1.535 -1.535 ... -0.24 xi_tilde_raw (chain, draw, market, inside_product) float64 12MB ... ... ... xi_j (chain, draw, inside_product) float64 768kB -0.... sigma_xi (chain, draw) float64 32kB 0.2155 ... 0.7866 xi_tilde (chain, draw, market, inside_product) float64 12MB ... xi (chain, draw, market, inside_product) float64 12MB ... s_inside (chain, draw, market, inside_product) float64 12MB ... s_outside (chain, draw, market) float64 512kB 0.7729 ... ... Attributes: created_at: 2026-05-26T06:54:35.235131+00:00 arviz_version: 0.23.0 -

<xarray.Dataset> Size: 340kB Dimensions: (chain: 4, draw: 1000) Coordinates: * chain (chain) int64 32B 0 1 2 3 * draw (draw) int64 8kB 0 1 2 3 4 5 ... 995 996 997 998 999 Data variables: (12/13) depth (chain, draw) uint64 32kB 2 0 1 6 5 10 ... 7 5 6 5 5 7 maxdepth_reached (chain, draw) bool 4kB False False ... False False index_in_trajectory (chain, draw) int64 32kB -1 0 0 -20 ... 53 -12 -14 57 logp (chain, draw) float64 32kB -6.706e+04 ... -704.8 energy (chain, draw) float64 32kB 6.903e+04 ... 900.7 energy_error (chain, draw) float64 32kB -14.84 0.0 ... 0.07156 ... ... step_size_bar (chain, draw) float64 32kB 0.5974 0.1441 ... 0.09203 mean_tree_accept (chain, draw) float64 32kB 0.6667 0.0 ... 0.9917 mean_tree_accept_sym (chain, draw) float64 32kB 2.044e-06 0.0 ... 0.9568 n_steps (chain, draw) uint64 32kB 3 1 3 63 31 ... 63 31 31 127 tuning (chain, draw) bool 4kB True True True ... True True diverging (chain, draw) bool 4kB False True True ... False False Attributes: created_at: 2026-05-26T06:54:35.245557+00:00 arviz_version: 0.23.0

fig, axs = plt.subplots(1, 2, figsize=(14, 4), sharey=True)

az.plot_posterior(

model.idata,

var_names=["alpha_pop"],

ax=axs[0],

)

axs[0].set_title("With instruments (IV)")

az.plot_posterior(

model_noiv.idata,

var_names=["alpha"],

ax=axs[1],

)

axs[1].set_title("Without instruments (no IV)")

plt.suptitle(

"Price coefficient: endogeneity bias pulls alpha toward zero",

fontsize=13,

y=1.02,

)

plt.tight_layout()

plt.show()

iv_mean = float(model.idata.posterior["alpha_pop"].mean())

noiv_mean = float(model_noiv.idata.posterior["alpha"].mean())

print(f"IV posterior mean: {iv_mean:.3f}")

print(f"no-IV posterior mean: {noiv_mean:.3f}")

print(f"Bias toward zero: {abs(iv_mean) - abs(noiv_mean):.3f}")

print("\nWithout instruments the model underestimates price sensitivity,")

print("producing unrealistically small elasticities.")

IV posterior mean: -0.328

no-IV posterior mean: -0.277

Bias toward zero: 0.051

Without instruments the model underestimates price sensitivity,

producing unrealistically small elasticities.

Note that \(\alpha\) is estimated on the cents scale (price × 100). Multiply by 100 to recover the dollar-scale coefficient comparable to Nevo’s \(\alpha \sim -30\).

6. Own-price elasticities and counterfactuals#

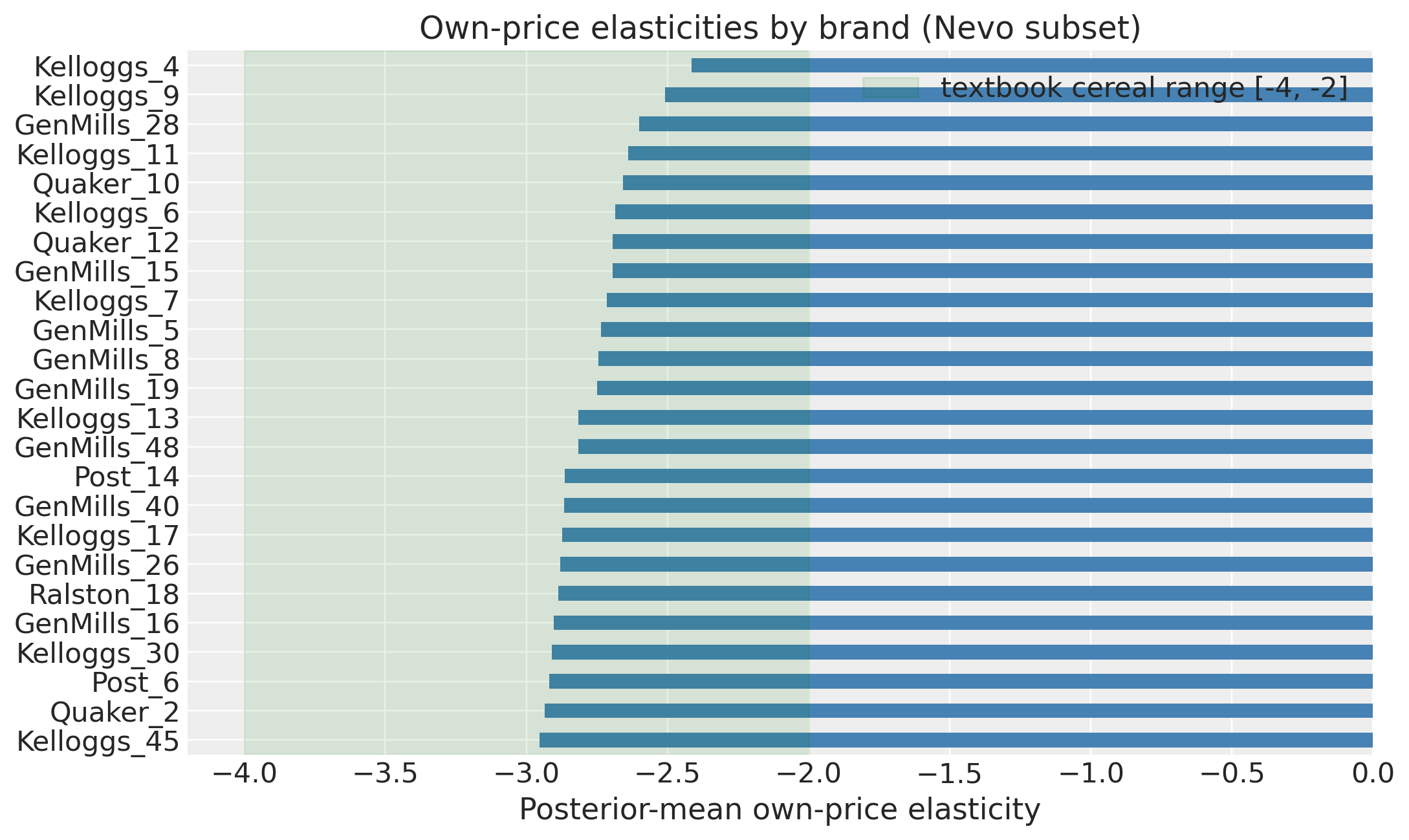

The headline test of any BLP demand estimator: do own-price elasticities land in a plausible range? For ready-to-eat cereal Nevo and the wider literature put the typical own-price elasticity in \([-2, -4]\).

elast = model.elasticities(at="mean", n_samples=400)

own_eps = pd.Series(

{

pname: float(elast.values[:, j, j].mean())

for j, pname in enumerate(model._inside_products)

}

).sort_values()

fig, ax = plt.subplots(figsize=(10, 6))

own_eps.plot(kind="barh", ax=ax, color="steelblue")

ax.axvspan(-4, -2, color="green", alpha=0.1, label="textbook cereal range [-4, -2]")

ax.set_xlabel("Posterior-mean own-price elasticity")

ax.set_title("Own-price elasticities by brand (Nevo subset)")

ax.legend()

plt.tight_layout()

plt.show()

print(

f"Range: [{own_eps.min():.3f}, {own_eps.max():.3f}]. "

f"Median: {own_eps.median():.3f}."

)

Range: [-2.954, -2.415]. Median: -2.782.

# Counterfactual: 10% price hike on the largest brand, panel-wide

target = own_eps.idxmin() # most elastic — biggest expected response

print(f"Applying a 10% price hike to {target} (own-ε = {own_eps[target]:.2f})")

baseline = model.counterfactual_shares(price_change=None, n_samples=400)

shocked = model.counterfactual_shares(price_change={target: 0.10}, n_samples=400)

base_s = baseline["s_inside"].mean(dim="sample").values

shocked_s = shocked["s_inside"].mean(dim="sample").values

delta = shocked_s - base_s

j_target = model._inside_products.index(target)

print(f"\nMarket-average share of {target}:")

print(f" baseline: {base_s[:, j_target].mean():.4f}")

print(f" shocked: {shocked_s[:, j_target].mean():.4f}")

print(f" Δ: {delta[:, j_target].mean():+.4f}")

# Where did the lost share go? Top rivals + outside good.

delta_outside = (

shocked["s_outside"].mean(dim="sample") - baseline["s_outside"].mean(dim="sample")

).values.mean()

rival_changes = pd.Series(

{

pname: float(delta[:, j].mean())

for j, pname in enumerate(model._inside_products)

if pname != target

}

).sort_values(ascending=False)

print("\nLargest gainers among rivals (top 5):")

print(rival_changes.head().to_string())

print(f"\nOutside-good Δshare: {delta_outside:+.4f}")

Applying a 10% price hike to Kelloggs_45 (own-ε = -2.95)

Market-average share of Kelloggs_45:

baseline: 0.0101

shocked: 0.0077

Δ: -0.0024

Largest gainers among rivals (top 5):

Kelloggs_6 0.000197

Kelloggs_11 0.000122

Post_14 0.000100

GenMills_8 0.000090

GenMills_19 0.000090

Outside-good Δshare: +0.0010

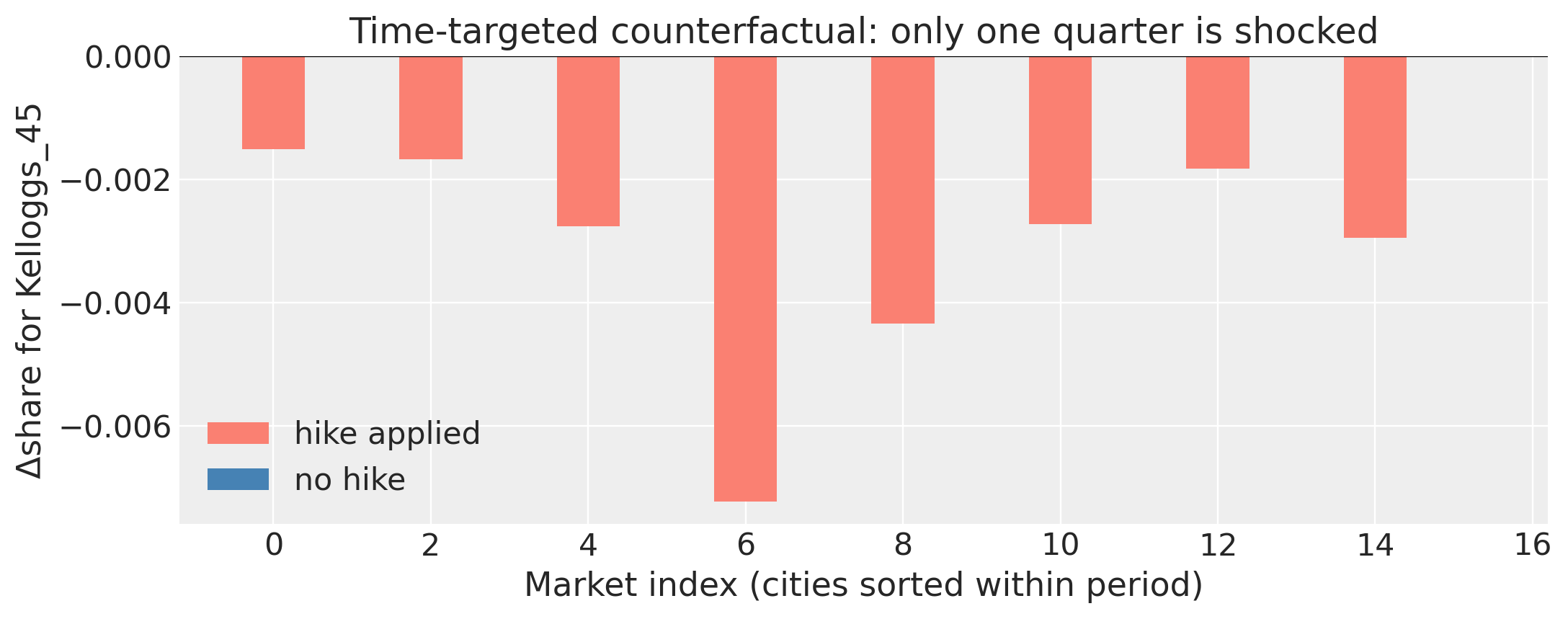

# Time-targeted counterfactual: same hike, but applied only in period 1.

period_target = sorted(df["period"].unique())[0]

shocked_q = model.counterfactual_shares(

price_change={target: 0.10}, periods=[period_target], n_samples=400

)

period_coord = shocked_q.coords["period"].values

in_window = period_coord == period_target

delta_in = (

(shocked_q["s_inside"] - baseline["s_inside"])

.mean(dim="sample")

.values[:, j_target]

)

fig, ax = plt.subplots(figsize=(10, 4))

markets = np.arange(model._M)

ax.bar(markets[in_window], delta_in[in_window], color="salmon", label="hike applied")

ax.bar(markets[~in_window], delta_in[~in_window], color="steelblue", label="no hike")

ax.axhline(0, color="k", lw=0.8)

ax.set_xlabel("Market index (cities sorted within period)")

ax.set_ylabel(f"Δshare for {target}")

ax.set_title("Time-targeted counterfactual: only one quarter is shocked")

ax.legend()

plt.tight_layout()

plt.show()

print(f"\nIn period {period_target}: mean Δ = {delta_in[in_window].mean():+.4f}")

print(

f"Outside period {period_target}: max |Δ| = {np.abs(delta_in[~in_window]).max():.2e} "

"(must be exactly zero — sanity check that the mask is correct)"

)

In period 353: mean Δ = -0.0031

Outside period 353: max |Δ| = 0.00e+00 (must be exactly zero — sanity check that the mask is correct)

7. Taste profiles across markets#

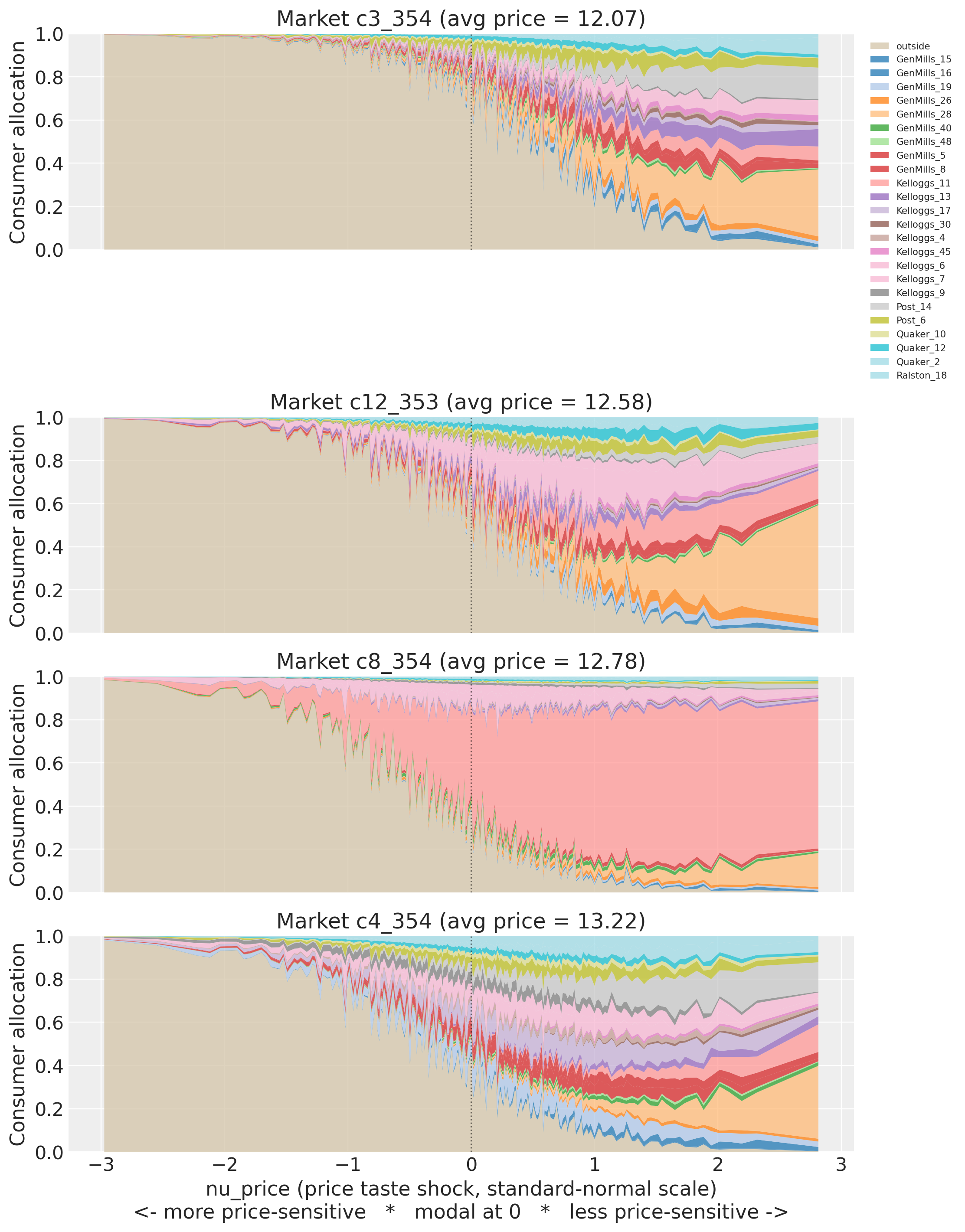

The model integrates over consumer taste types to predict aggregate shares. With three random coefficients each consumer is a vector \(\bm{\nu}_i = (\nu_{\text{price}}, \nu_{\text{sugar}}, \nu_{\text{mushy}})\). The stacked area chart below sorts consumers along \(\nu_{\text{price}}\) only and gives a price-marginal view: at each x-coordinate the other two taste dimensions vary across the Halton grid. The fully multi-dimensional buyer characterisation comes from the heatmap further down (Lens 1).

taste_profiles.plot_taste_profile_stacked(model, n_samples=200);

profiles = taste_profiles.taste_type_demand_share(model, n_samples=200)

nu_price = taste_profiles.consumer_taste_grid(model)["price"].to_numpy()

baseline = {

"sensitive": f"{(nu_price < -1).mean():.2f}",

"modal": f"{((nu_price >= -1) & (nu_price <= 1)).mean():.2f}",

"insensitive": f"{(nu_price > 1).mean():.2f}",

}

print("Share of inside-good demand by taste-type bucket:\n")

print(profiles.to_string(index=False, float_format=lambda x: f"{x:6.3f}"))

print(f"\nHomogeneous baseline (flat logit): {baseline}")

Share of inside-good demand by taste-type bucket:

market avg_price sensitive_pct modal_pct insensitive_pct

c1_353 13.171 0.022 0.657 0.321

c1_354 12.892 0.034 0.676 0.291

c11_353 12.588 0.032 0.670 0.298

c11_354 13.100 0.024 0.658 0.318

c12_353 12.579 0.027 0.665 0.309

c12_354 12.171 0.031 0.664 0.305

c3_353 12.587 0.024 0.645 0.332

c3_354 12.071 0.018 0.607 0.375

c4_353 12.075 0.053 0.718 0.229

c4_354 13.221 0.043 0.705 0.252

c5_353 12.471 0.026 0.647 0.326

c5_354 12.771 0.028 0.638 0.335

c7_353 12.196 0.050 0.702 0.248

c7_354 12.600 0.056 0.719 0.224

c8_353 13.179 0.023 0.650 0.327

c8_354 12.783 0.041 0.716 0.243

Homogeneous baseline (flat logit): {'sensitive': '0.16', 'modal': '0.68', 'insensitive': '0.16'}

Reading the four markets#

Twenty-four brands is a lot of colour. Three patterns are worth picking out:

Cheapest market (low avg price): inside demand is diversified. The outside good (beige) shrinks quickly as \(\nu\) rises and several brands take meaningful slices. No single product dominates because at this price level the characteristic differences between brands matter more than any individual brand’s unobserved-quality advantage.

A one-brand-dominates market. Look for the panel where, at \(\nu > 0\), almost the entire stack is a single colour. This signature appears when one product has a very large posterior \(\xi\) in that market (high unobserved quality given its price). The model can only explain a 40%+ inside share for one brand at moderate price by attributing it to \(\xi\); consumers who can tolerate the price then almost all pick that brand. This is the model recovering a brand-level outlier from the share data alone.

Most expensive market: outside good never disappears. Even at \(\nu \approx 2\) the outside good still holds 30–50% of the allocation. Price sensitivity remains binding at the top of the \(\nu\) distribution. Compare this to the cheapest market, where the outside good is almost gone by \(\nu = 0\).

The demand-share table below quantifies the same story. The flat-logit baseline (no random coefficients) would be {sensitive: 0.16, modal: 0.68, insensitive: 0.16}, the population weights of the three \(\nu\) buckets. Wherever the observed insensitive_pct exceeds 0.16, the random coefficient on price is doing real work: that market’s inside demand leans on consumers who can absorb the price, and a flat-logit substitution pattern would mis-predict who switches when prices change.

Who is the average inside-good buyer?#

The stacked plot is qualitative. To characterise each market by a full taste vector with posterior uncertainty, compute

per posterior sample, for each dimension \(d \in \{\text{price}, \text{sugar}, \text{mushy}\}\). One scalar per (sample, market, dimension) gives a posterior over “the average customer who actually buys in this market”, decomposed by taste axis.

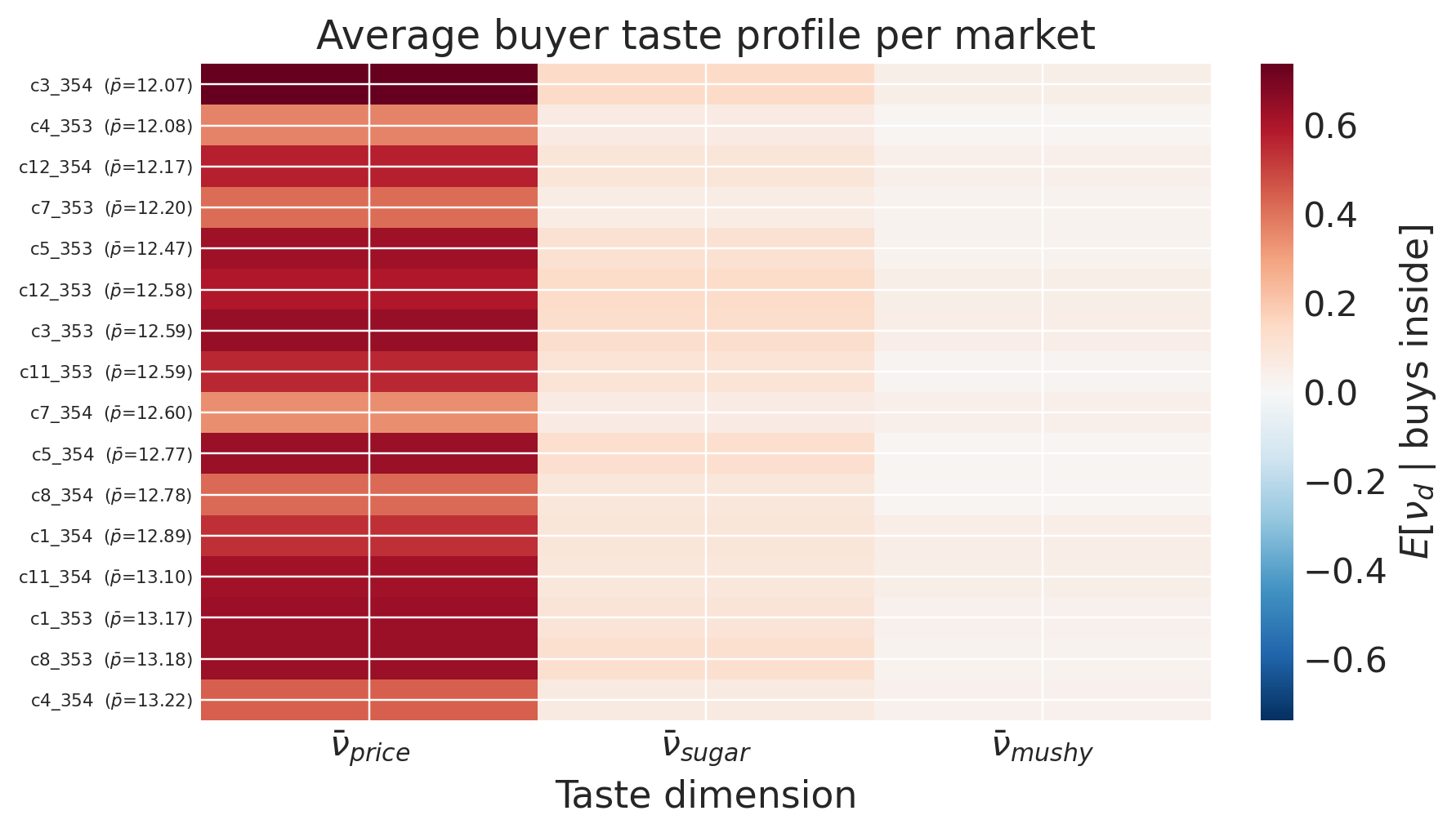

taste_profiles.plot_buyer_profile_heatmap(model, n_samples=300);

Each row is a market sorted by average cereal price; each column is one of the three taste dimensions. Red means the typical buyer scores above-modal on that dimension (price-insensitive, or strong positive preference for the characteristic). Blue means below-modal.

The \(\bar\nu_{\text{price}}\) column should shift from blue at the top (cheap markets attract price-sensitive buyers) to red at the bottom (expensive markets keep only insensitive buyers). The \(\bar\nu_{\text{sugar}}\) and \(\bar\nu_{\text{mushy}}\) columns then add the characteristic story on top: a row that is red on sugar but blue on mushy is a market whose buyers prefer sugary cereals and avoid mushy ones, on top of their price-tolerance position.

The scalar “average buyer \(\nu\)” picture said “this market is served by price-insensitive consumers”. The three-column picture says “this market is served by consumers who are price-insensitive and high-sugar preference and mushy-averse”. That is the multi-dimensional taste profile the BLP machinery is designed to recover.

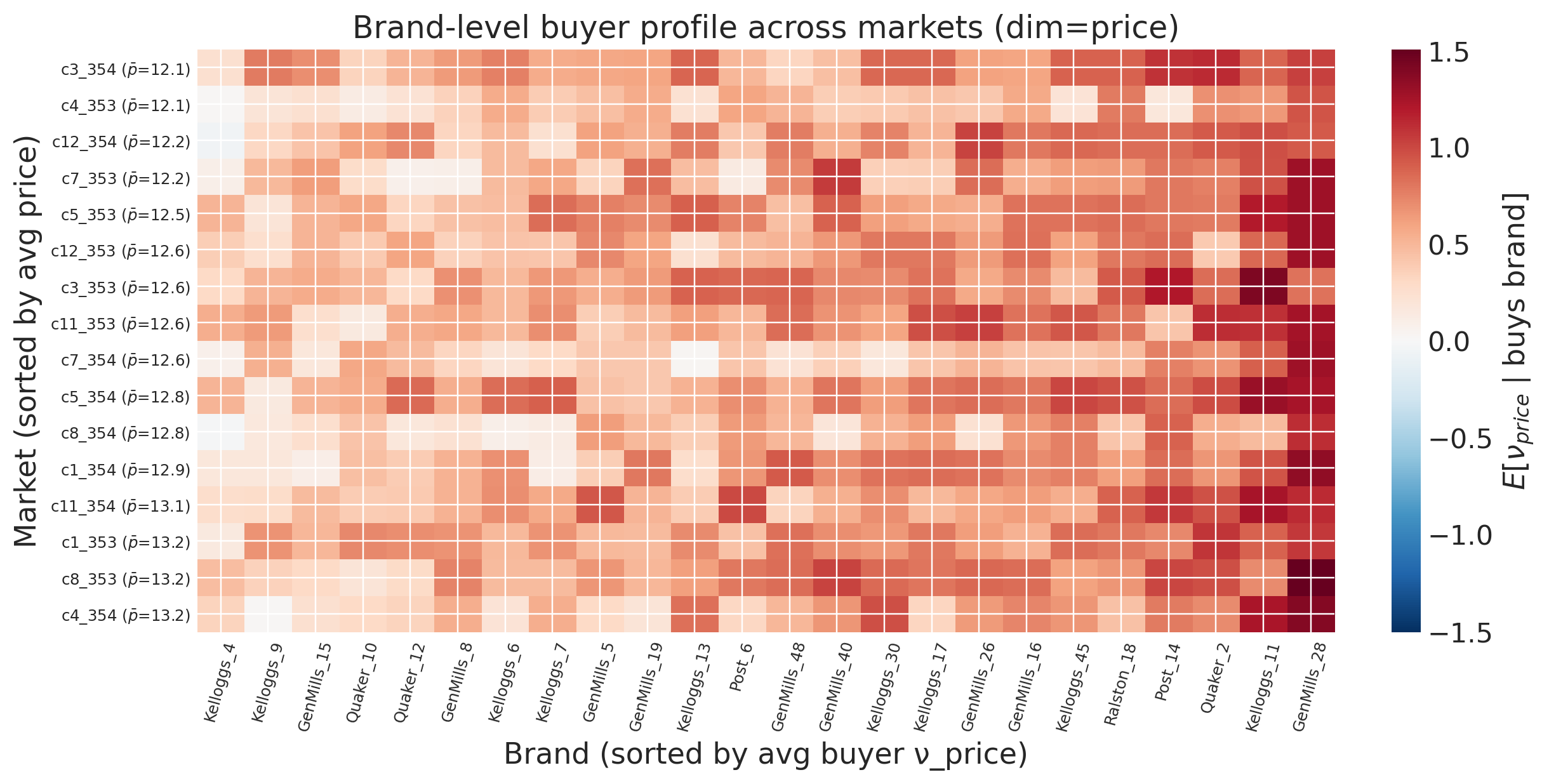

Brand-level buyer profile (price dimension)#

The heatmap above gives the market-level taste profile. We can also drill into individual brands: in each market, who is the typical buyer of each brand? The same construction restricted to a single product gives

To keep the visualisation 2D we restrict to the price dimension (\(d = \text{price}\)). The same construction extends to sugar and mushy by changing the slice of model._halton.

taste_profiles.plot_brand_buyer_heatmap(model, n_samples=200, dim=0);

Brands on the left of the heatmap (blue) serve more price-sensitive consumers; brands on the right (red) serve insensitive consumers. Two things to look for:

Vertical stripes. A brand whose column is uniformly coloured serves the same kind of customer everywhere. A brand whose column shifts colour from market to market changes its customer profile based on the local competitive context.

Horizontal stripes. A market whose row varies wildly across brands offers products that serve different consumer slices; a market whose row is flat offers a homogeneous brand mix targeting one type of buyer.

Combined with the market-level \(\bar\nu_m\) from the previous lens, this gives a two-tier characterization: the average buyer in each market, and the buyer mix across brands within that market.

8. Caveats#

Subset. We fit on 8/47 cities. The full panel would deliver more statistical power, but the qualitative result (textbook elasticity range, identified \(\rho\)) is robust.

Outside-good

n_jt. Nevo’s published data lacks per-market serving counts. Then=1,000placeholder enters only the heteroskedastic-Normal variance term, so it does not bias point estimates. It does compress posterior intervals slightly relative to a fit with true serving counts.Demographics. Nevo’s original paper enriches consumer heterogeneity with demographic interactions (income, age, child presence) drawn from CPS. Our model uses the basic mixed-logit form with a random coefficient on price only.

Simulated data. Nevo (2000) states the Practitioner’s Guide dataset is simulated data calibrated to the cereal market. The real empirical results are in Nevo (2001, Econometrica). Results here should not be cited as findings from real market observations.

%load_ext watermark

%watermark -n -u -v -iv -w -p pymc_marketing,nutpie,pymc

Last updated: Tue May 26 2026

Python implementation: CPython

Python version : 3.12.12

IPython version : 9.8.0

pymc_marketing: 0.19.3

nutpie : 0.16.8

pymc : 5.28.2

matplotlib : 3.10.8

pandas : 2.3.3

pymc_marketing: 0.19.3

arviz : 0.23.0

pymc_extras : 0.10.0

numpy : 2.3.5

Watermark: 2.5.0